Money has gone into Interactive Brokers (IBKR), and one day you may want to take part of it out. Most people instinctively think of wiring it back to a bank and converting it back to New Taiwan dollars.

But if you originally sent USDC in from on-chain and want to turn it back into USDC in your wallet, the FluidKey route can be run in reverse.

The previous article covered funding IBKR with USDC. This one covers the opposite direction: withdrawing dollars from IBKR over ACH to your same-name FluidKey account, then automatically converting them into USDC on Base. I ran a real transaction and documented it.

How the route works

FluidKey connects to fiat rails through Bridge (acquired by Stripe). After KYC, you get a USD account in your own name. IBKR’s ACH withdrawal sends money into that account; FluidKey receives the dollars and converts them into USDC on Base.

In one line: IBKR → (ACH withdrawal) → FluidKey USD account → automatic conversion to USDC (Base).

There is one point that is exactly opposite from deposits and easy to mix up. When funding IBKR, you initiate from FluidKey and push money to IBKR; when withdrawing, the direction is reversed: IBKR actively pushes the money by ACH to your FluidKey bank account. What you need to do is enter FluidKey’s account details correctly in IBKR’s withdrawal settings.

The actual steps

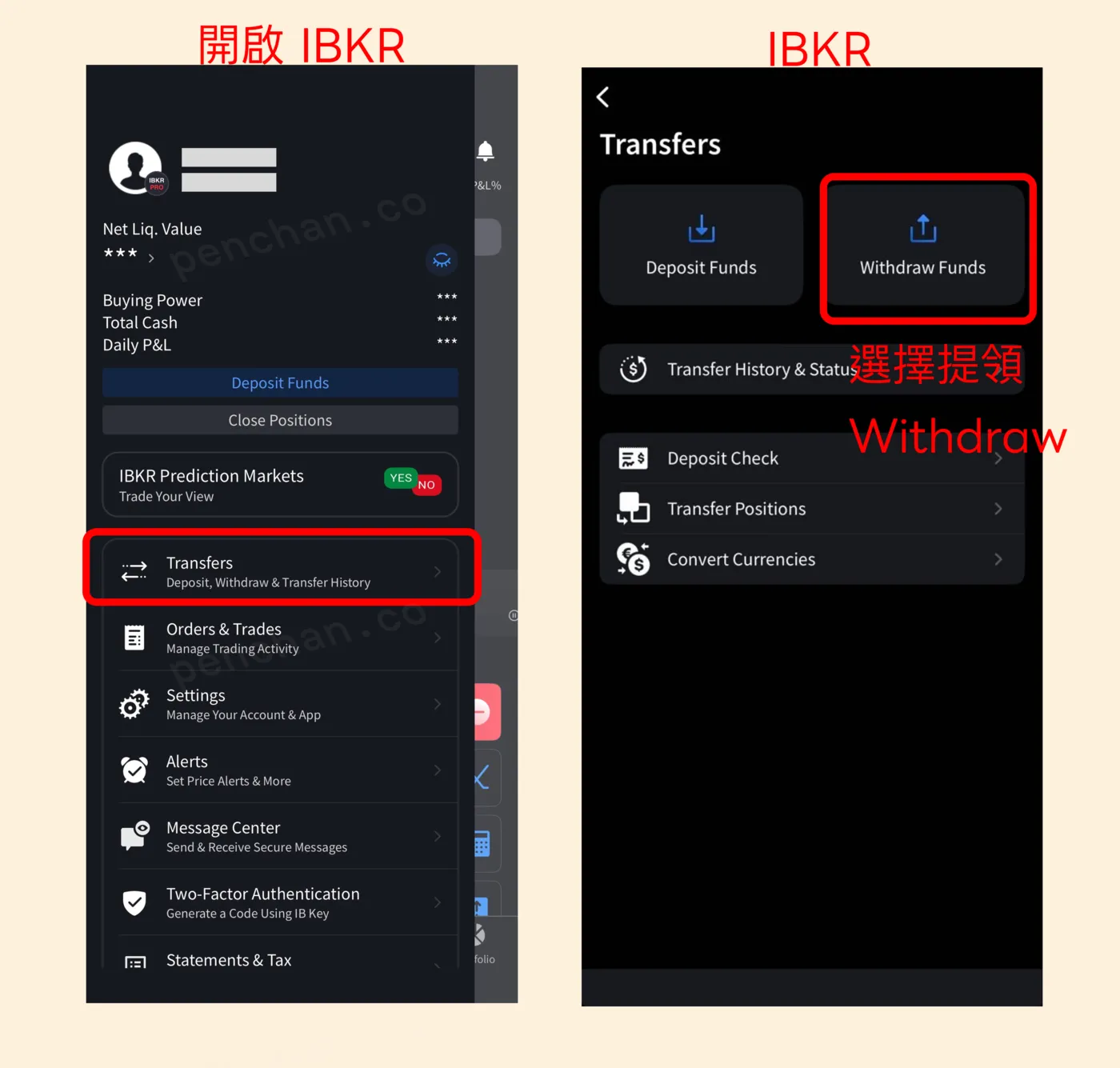

Step 1: Start the withdrawal in IBKR

Open IBKR, go to Transfers (Deposit, Withdraw & Transfer History are all here), then choose Withdraw Funds.

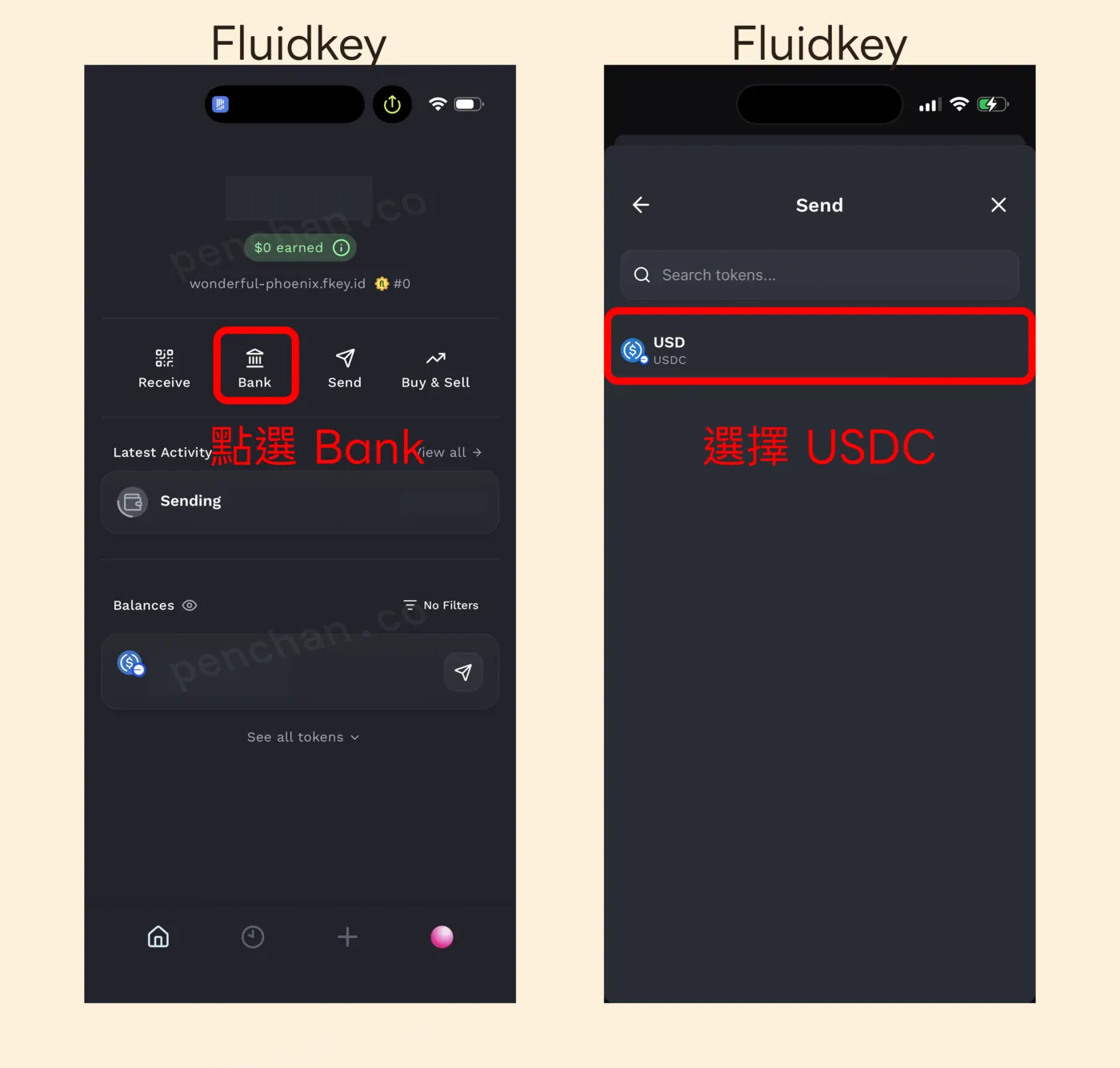

Step 2: Get your USD account details from FluidKey

In FluidKey, tap Bank, choose USD (USDC), and you will see a set of Bank Details: account holder name, Routing Number, Account Number, with Lead Bank as the receiving bank. This is the information you will enter back into IBKR. The account holder name must be your own; that is the key to whether the same-name check passes.

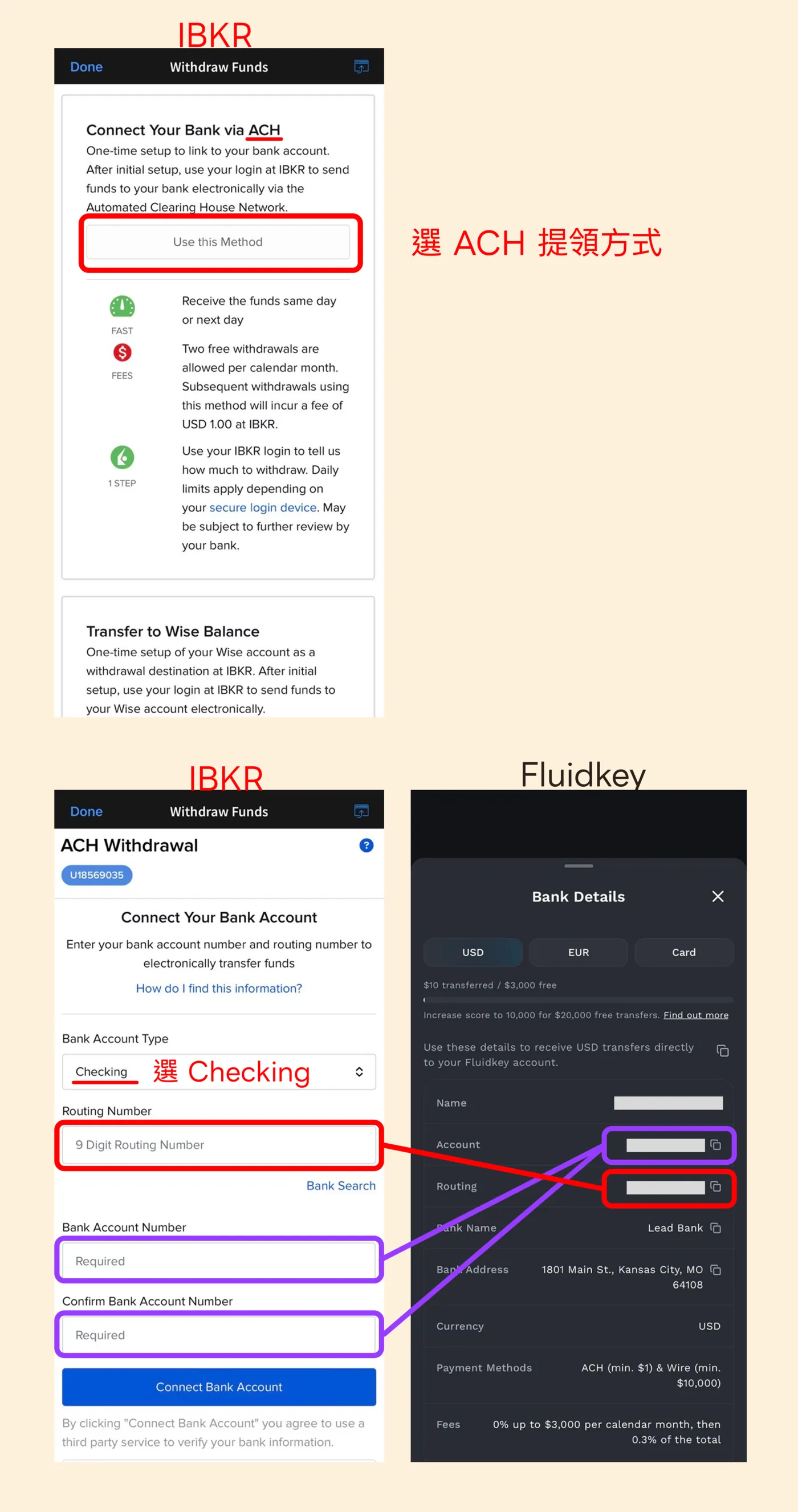

Step 3: In IBKR, choose ACH and enter FluidKey’s account details

Choose Connect Your Bank via ACH as the withdrawal method (the screen explains that funds arrive same day or next business day, that there is a monthly number of free withdrawals, and that fees apply after that; the actual rule depends on what the screen shows at the time).

Then, in the ACH Withdrawal Connect Your Bank Account form, set Bank Account Type to Checking, paste the Routing Number and Account Number that FluidKey provided, and tap Connect Bank Account. Confirm the amount and submit.

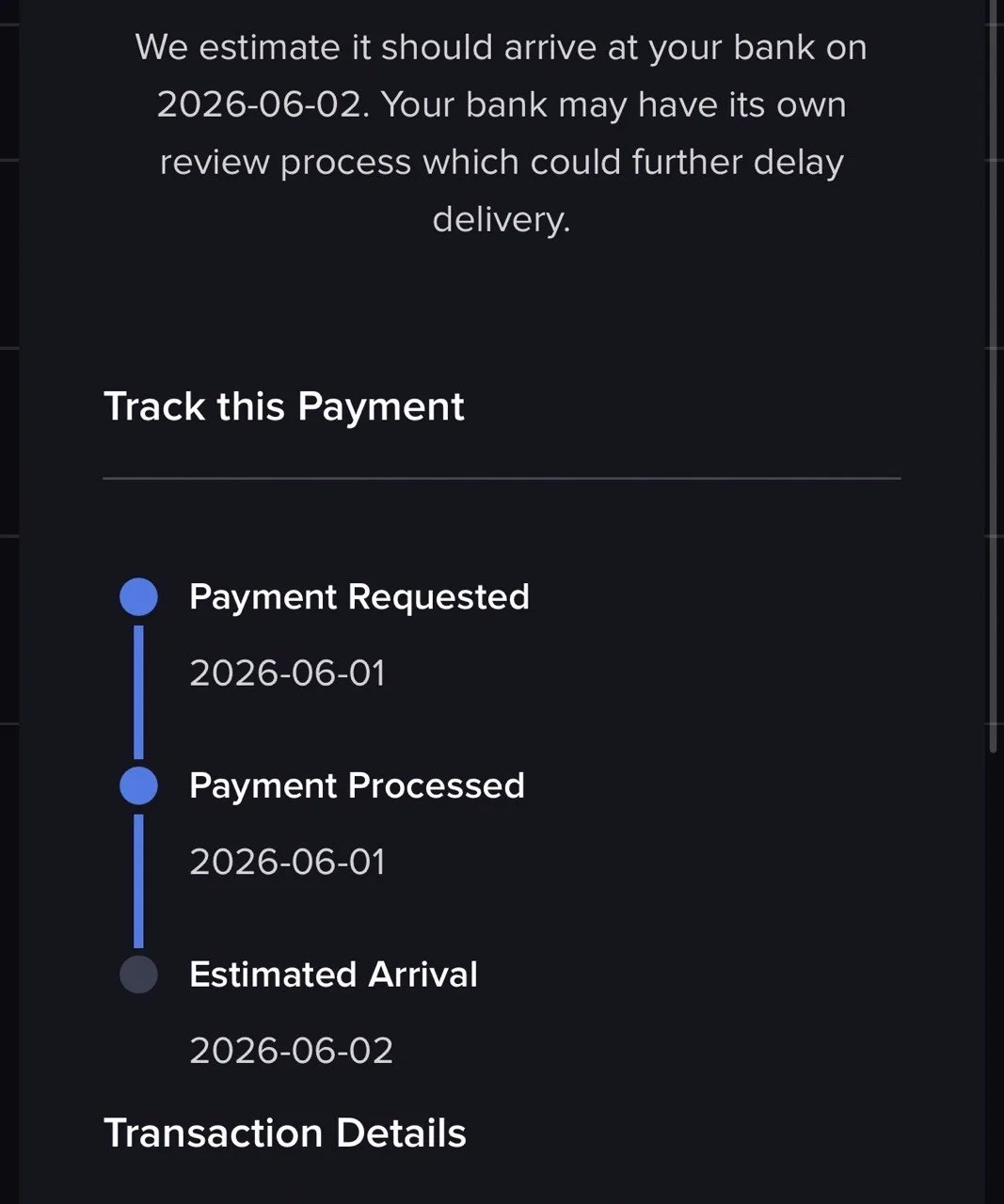

Step 4: Confirm submission and track the payment

After submission, IBKR gives you a receipt where you can track the payment: Payment Requested, Payment Processed, and the estimated arrival date. For this transaction, I submitted it on 6/1, and IBKR estimated arrival on 6/2.

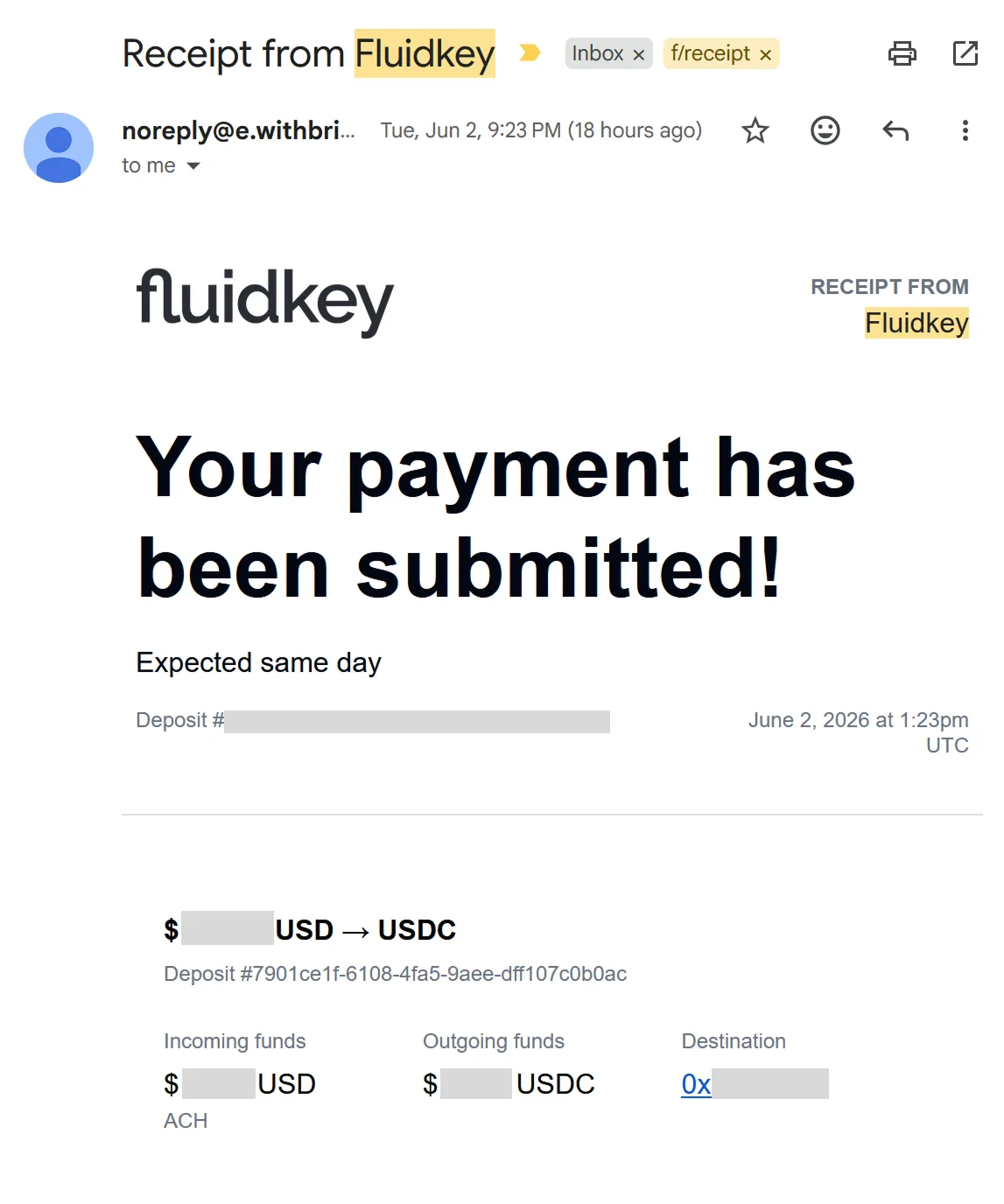

Step 5: FluidKey receives it and automatically converts it into USDC

Once the money reaches FluidKey, you receive a confirmation email (sent by Bridge) showing USD → USDC and the destination address on Base. The money is back on-chain.

This actual test: 10 USDC, withdrawal submitted in IBKR at 22:27 on 6/1, USDC received in FluidKey on Base at 21:23 on 6/2, roughly one day, landing the next day. One successful run does not mean every run for every person will be this smooth; amount, timing, and account review can all stretch the timeline.

Risks and red lines

Names have to match. IBKR only withdraws to an account in your own name, and the FluidKey USD account is also opened after KYC in your own name. If the names do not match, it gets returned.

Withdrawal hold period. IBKR applies withdrawal holds to recently deposited funds. For funds deposited via stablecoins, the official listing shows a 30-business-day hold, so newly deposited money cannot be withdrawn immediately. The money you withdraw should be funds that have already sat there for a while and passed the hold period.

Withdrawal count and fees. IBKR gives a monthly number of free ACH withdrawals, then charges after that; on FluidKey’s side, the free allowance (deposits and withdrawals combined) is followed by a 0.3% fee. The actual numbers should be based on what the two interfaces show at the time.

Converting back to stablecoins does not mean there is no tax. Turning dollars back into USDC, or later cashing out again, may still involve reporting and tax on gains. This route may not pass through a Taiwan bank’s foreign-exchange settlement, but that does not mean there are no tax issues. A privacy tool reduces on-chain linkage, not reporting obligations.

One more processor in the chain. The funds are actually handled by Bridge, so the chain of responsibility has one more link than a direct wire.

Offshore, without local supervision. FluidKey is not supervised by Taiwan’s FSC, and assets are not protected by deposit insurance; if you lose your self-custody private keys, no one can rescue them.

Invite links and a reminder

This route uses two services: FluidKey (stablecoin wallet) and IBKR (broker). Both are referral links; if you sign up through them, Penchan receives a referral reward, and your fees are not affected.

If you want to go the other way and fund IBKR with USDC to buy U.S. stocks, see this illustrated guide; if you want to understand what FluidKey is first, see this breakdown.

The first time, always run the whole route with an amount small enough that you would not mind losing it, confirm the name match and arrival, then scale up.

Deposits being smooth and withdrawals being smooth is what makes this route a real loop. After running this transaction, what felt most solid was seeing every step with my own eyes: how money moves from on-chain into the broker, then how it returns on-chain along the same path. The remaining variables are still whether residents of Taiwan or other regions can open the accounts and pass review; that has to be tested individually.