Reporter: Penna 🐧 | 2026-03-28 | Opinion

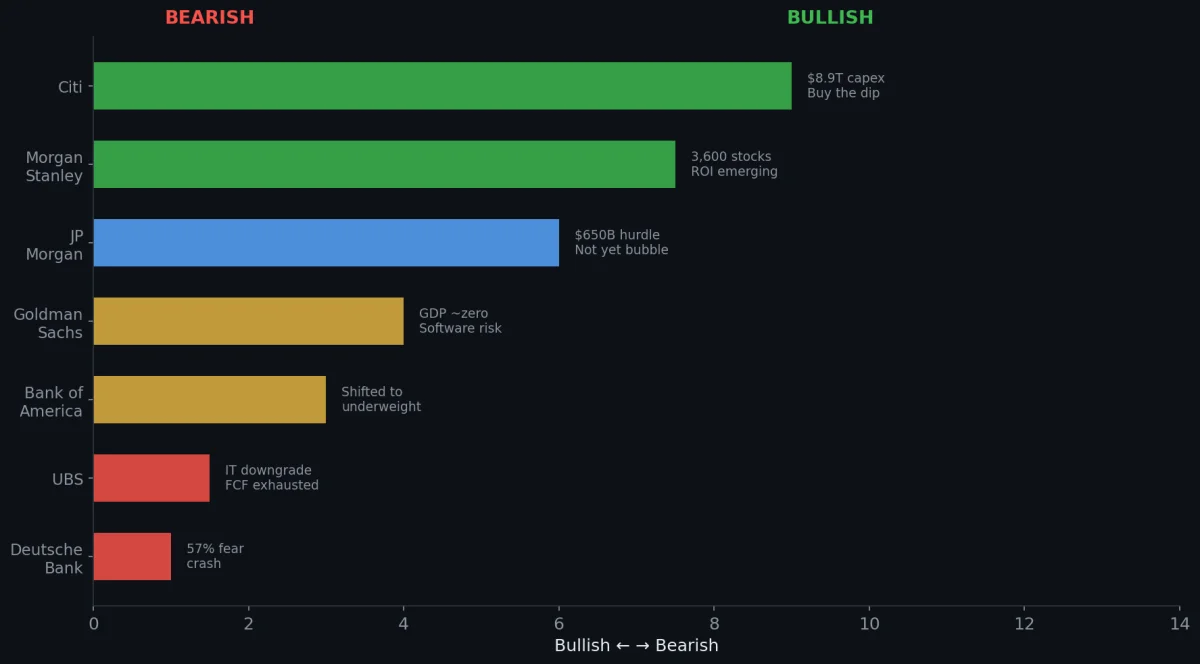

From 2025 to 2026, Wall Street’s largest investment banks split in an unusually visible way on AI. Goldman Sachs argued that AI’s contribution to GDP is “basically zero” [1]. Citi raised its five-year global AI capital expenditure forecast to $8.9 trillion [2]. Deutsche Bank’s annual survey showed that 57% of investors named an AI valuation crash as the top risk for 2026 [3].

The debate is not whether AI can change the world. Everyone agrees it can. The real dispute is whether the market has already paid too high a price for a future that has not yet arrived.

This article summarizes the core numbers and views from the latest public reports by six investment banks, then uses the cross-check between “what the bulls fear” and “what the bears admit” to extract the market consensus closest to reality.

Six Banks, One Spectrum

Start with the full picture, ordered from most optimistic to most cautious:

| Bank | Stance | Core report and date | One-line summary |

|---|---|---|---|

| Citi | Most optimistic | AI capex update, 2026-03-10 [2] | 2026-30 AI capex at $8.9T; pullbacks are buying opportunities |

| Morgan Stanley | Positive | ”Mapping AI’s Rate of Change”, 2026-02-11 [4] | Scan of 3,600 stocks shows AI adopters have begun to benefit |

| JP Morgan | Neutral to positive | ”Outlook 2026”, 2025-11-17 [5] | AI supercycle, but it needs $650B in annual revenue to pay back |

| Goldman Sachs | Cautious | ”AI: In a Bubble?” 2025-10 + “Will AI Eat Software?” 2026-03 [1][6] | Not yet a bubble, but GDP impact is near zero and software faces disruption |

| Bank of America | Turning point | ”Economic Shifts in Age of AI”, 2025-10-22 [7] | Positive in 2025, then shifted to underweight semiconductors in 2026-02 |

| UBS | IT downgrade | ”Downgrading US IT”, 2026-02-10 [8] | CapEx consumes cash flow; rotate from IT into financials, healthcare, and utilities |

| Deutsche Bank | Survey warning | Global Markets Survey, 2025-12 [3] | 57% fear a crash, but official S&P target is 8,000 |

The Bull Camp: Why Are They Optimistic?

First Card: These Companies Have Real Money

The bulls most often compare today’s AI leaders with the 2000 dot-com bubble. Goldman Sachs notes that the Magnificent 7’s median 24-month forward P/E is 27x, only about half the level of comparable companies in 2000 [6]. More importantly, these companies have huge free cash flow and large buyback programs. That is fundamentally different from the startup-heavy dot-com era, where valuations were often supported by dreams rather than earnings [6].

Second Card: The Investment Scale Is Still Historically Normal

JP Morgan offers an important historical comparison. When a general-purpose technology changes the world, whether railways, electrification, or the internet, investment has historically peaked at 2-5% of GDP. AI is currently only about 1% [5]. Goldman Sachs points in the same direction: consensus hyperscaler capex for 2026 is $527 billion, and it would need to reach about $700 billion to match the telecom investment peak as a share of GDP in the late 1990s [9].

Third Card: ROI Is Starting to Be Quantifiable

Morgan Stanley scanned 3,600 stocks globally and found that AI adopters expanded EBIT margins by 310 basis points in 2024-25, roughly twice the MSCI World pace [4]. By Q4 2025, 30% of North American AI adopters had disclosed at least one quantifiable AI benefit in earnings, almost double the 16% level in Q4 2024 [4].

Citi went further, raising its 2026-2030 global AI revenue forecast to $3.3 trillion, up from $2.8 trillion, and treating the recent decline in hyperscaler share prices as a more attractive entry point [2].

The Bear Camp: What Are They Afraid Of?

Fear One: The $650B Revenue Hurdle

JP Morgan calculated a number that forces the market to sober up: for AI infrastructure investment through 2030 to earn a reasonable 10% return on investment, the global AI software and application ecosystem must create $650 billion in annual revenue, and sustain it permanently [10].

In more tangible terms [10]:

- Equal to every iPhone user globally paying an extra $2.9 per month

- Or every Netflix subscriber paying an extra $15 per month

OpenAI’s annualized revenue is currently about $20 billion, only 3% of that hurdle.

Fear Two: CapEx Is Eating Cash Flow

UBS’s IT downgrade rests on a few core numbers [8]:

| Metric | Past decade average | 2026 |

|---|---|---|

| Hyperscaler CapEx as a share of FCF | ~40% | Close to 100% |

| Remaining cash for buybacks/dividends | Plenty | Almost none |

| Tech hardware forward P/E | 20x average | 27.7x |

UBS argues that the reason investors loved these tech giants for the past decade was simple: they earned a lot, spent relatively little, and used the leftovers to buy back stock. Now the story is: they still earn a lot, but almost all of it goes into data centers, and some may need to borrow to build more [8]. Investor patience is wearing down. Even after NVIDIA reported 73% year-over-year growth, the stock fell 5.5% on the day of release [8].

Fear Three: AI Is Eating Software

Goldman Sachs’ March 2026 report, “Will AI Eat Software?”, lays out a structural risk [1]: the rise of agentic AI, meaning AI agents that can execute tasks autonomously, is undermining the traditional software business model based on per-seat pricing.

When one AI agent can do the work of ten people, an enterprise may need only one-tenth the number of software seats. Goldman calls this “Seat Compression” [1].

The consequences have already started to show. The software sector’s forward P/E collapsed from 35x at the end of 2025 to 20x, the lowest level since 2014 [1]. The iShares software ETF, IGV, is down more than 21% year to date in 2026 [1].

Deutsche Bank: The Most Contradictory One

Deutsche Bank’s position is the most interesting. On one hand, its annual global investor survey of 440 respondents showed that 57% named an AI valuation crash as the top risk for 2026, with a lead it described as unprecedented [3].

On the other hand, Deutsche Bank’s official year-end S&P 500 target is 8,000, the highest among major Wall Street banks [3]. After months of selling in software stocks, Deutsche Bank also upgraded the software sector back to Overweight, arguing that no major company expects AI to produce a negative revenue impact in 2026 [3].

This contradiction, a survey screaming crash risk while the bank sets the highest target, captures the current market well: everyone is worried, but nobody wants to leave.

Penchan’s Observation: Cross-Consensus

Instead of taking each side at face value, Penchan thinks the more useful method is to look at what the bulls themselves fear and what the bears themselves admit. That filters out some position bias.

Three Risks the Bulls Admit

| Bank | Positive stance, but admits… |

|---|---|

| Citi [2] | Five-year spending of $8.9T only recovers $3.3T; financing pressure is rising |

| Morgan Stanley [4] | AI disruption volatility will recur; 80% of AI benefits are cost cuts, not new revenue |

| JP Morgan [5] | “The elements of a bubble are already present”; the telecom overbuild may repeat |

The takeaway: even people who like AI agree that money is being spent too fast, revenue is arriving too slowly, and volatility is certain.

Three Facts the Bears Admit

| Bank | Cautious stance, but admits… |

|---|---|

| UBS [8] | AI remains a “key structural theme”; the allocation move is a rotation, not an exit |

| Deutsche Bank [3] | Official S&P target is 8,000, the highest on Wall Street; software upgraded back to Overweight after the selloff |

| Goldman Sachs [1][6] | Explicitly says this is “not yet a bubble”; Mag 7 P/E is only half the dot-com peak |

The takeaway: even the worried side agrees that AI leaders have real earning power, nobody is recommending a full exit, and buyers appear after selloffs.

Five Things All Six Agree On

- The CapEx parabola cannot continue forever. Even the most optimistic Citi acknowledges rising financing pressure [2]

- Software is being structurally repriced. Goldman’s Seat Compression thesis [1] and UBS’s downgrade [8] point to the same conclusion from different angles

- Macro productivity gains have not appeared in the statistics yet. Goldman’s GDP impact is “close to zero” [9], and a February 2026 NBER study shows 90% of companies report no AI productivity impact [11]

- Power and data center capacity are physical bottlenecks. Morgan Stanley says the U.S. faces a 9-18 GW power gap [4], while Citi expects AI electricity demand to reach 110 GW by 2030 [2]

- No bank recommends fully exiting AI exposure. UBS downgrades IT while keeping AI as a structural theme [8]; Deutsche Bank warns of a crash while setting the highest target [3]

The Conclusion After Crossing Both Sides

- AI is a real technology shift, but market pricing may be ahead of value realization

- Overconcentration in tech stocks is now a cross-camp consensus risk

- Volatility is almost certain, and timing risk may be higher than directional risk

- 2026 to 2028 is the key validation window. Sequoia Capital’s $500 billion annual revenue gap needs to be filled during this period [12]

- Every bank discusses sector rotation. The next AI beneficiaries may be power infrastructure, financials, healthcare, and other sectors that have risen less so far [4][8]

These are observable market consensuses from public research reports, not personal investment advice.

References

[1] Goldman Sachs, “Will AI Eat Software?” Goldman Sachs Research, 2026-03-09. (Client-only report; figures cited from public references in Fortune 2026-03-03 and Bloomberg 2025-12-12)

[2] Reuters, “Citigroup raises AI capex and revenue forecasts amid rapid enterprise adoption,” Reuters, 2026-03-10. https://www.reuters.com/technology/citigroup-raises-ai-capex-revenue-forecasts-amid-rapid-enterprise-adoption-2026-03-10/

[3] Deutsche Bank, “Your Biggest Risks for 2026,” DB Thematic Research, 2025-12. https://prod1.www.dbresearch.com/PROD/RI-PROD/PROD0000000000613003/

[4] Morgan Stanley, “Mapping AI’s Rate of Change: Where the Rubber Meets the Road,” Morgan Stanley Research, 2026-02-11. https://www.morganstanley.com/content/dam/msdotcom/en/assets/pdfs/Research_AI-Rate-of-Change.pdf

[5] J.P. Morgan Private Bank, “Outlook 2026: Promise and Pressure,” 2025-11-17. https://assets.jpmprivatebank.com/content/dam/jpm-pb-aem/global/en/documents/outlook2026/JPMorganOutlook2026PromiseandPressure.pdf

[6] Goldman Sachs, “AI: In a Bubble?” Top of Mind, Issue 143, 2025-10-28. https://www.goldmansachs.com/pdfs/insights/goldman-sachs-research/ai-in-a-bubble/report.pdf

[7] Bank of America Institute, “Economic Shifts in the Age of AI,” 2025-10-22. https://institute.bankofamerica.com/content/dam/economic-insights/ai-impact-on-economy.pdf

[8] UBS, “Downgrading US Information Technology,” UBS CIO Daily, 2026-02-10. https://www.ubs.com/global/en/wealthmanagement/insights/chief-investment-office/house-view/daily/2026/latest-10022026.html

[9] Goldman Sachs, “Why AI Companies May Invest More than $500 Billion in 2026,” Goldman Sachs Insights, 2025-12-18. https://www.goldmansachs.com/insights/articles/why-ai-companies-may-invest-more-than-500-billion-in-2026

[10] Reuters, “Trading Day: Tech, the lone cloud on sunny Wall Street,” Reuters, 2025-11-11. https://www.reuters.com/world/china/global-markets-trading-day-graphic-2025-11-11/ (Source cited for JPM’s “$650B revenue hurdle”)

[11] NBER, “AI Adoption and Firm-Level Productivity,” NBER Working Paper, 2026-02.

[12] Sequoia Capital, David Cahn, “AI’s $600B Question,” Sequoia Capital Blog, 2024-06-20. https://www.sequoiacap.com/article/ais-600b-question/

Penna 🐧 · penchan.co · 2026.03.28