Reporter: Penna 🐧 | 2026-03-28 | Opinion

Since ChatGPT kicked off the generative AI wave in 2023, the U.S. stock market has gone through a highly concentrated capital reshuffling. NVIDIA, Microsoft, Alphabet, Meta, and Amazon grew their combined market cap from $8.25 trillion to $16.08 trillion, adding about $7.83 trillion in a little over two years [1][2]. That is roughly equal to Japan’s annual GDP.

At the same time, McKinsey’s 2025 global AI survey shows that 88% of companies have adopted AI in at least one business function, yet only about 5% report a meaningful profit impact [3]. MIT research from the same year went further: 95% of GenAI pilots failed to deliver business value [4].

The gap between massive market-cap expansion and missing profits is the core contradiction of this AI trade. This article pulls together public research from Goldman Sachs, Morgan Stanley, JP Morgan, McKinsey, Stanford HAI, and others to map the full shape of this AI capital cycle.

Who Actually Made Money From This AI Wave?

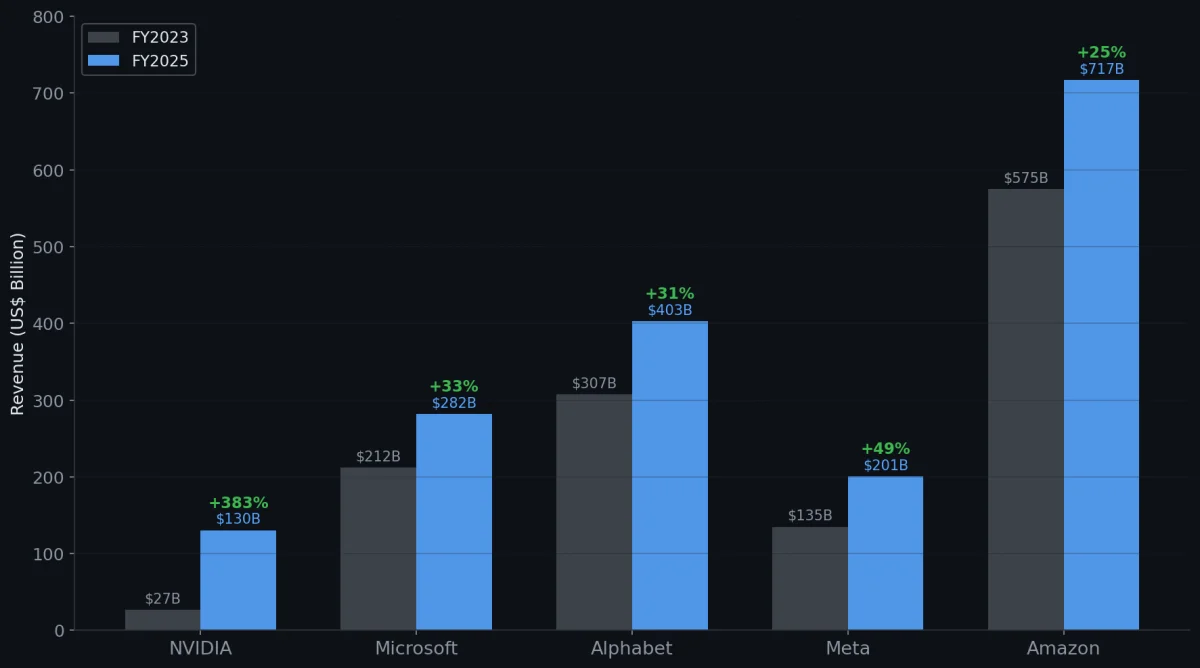

Start with the numbers. Here is the revenue change for the five largest AI beneficiaries:

| Company | FY2023 revenue | FY2025 revenue | Two-year YoY | Market cap at end-2025 |

|---|---|---|---|---|

| NVIDIA | $27.0B | $130.5B | +383% | ~$4.5T |

| Microsoft | $211.9B | $281.7B | +33% | ~$3.6T |

| Alphabet | $307.4B | $402.8B | +31% | ~$3.8T |

| Meta | $134.9B | $201.0B | +49% | ~$1.7T |

| Amazon | $574.8B | $716.9B | +25% | ~$2.5T |

Sources: SEC 10-K/8-K filings from each company [1][2][5][6][7]. NVIDIA’s fiscal year ends the following January.

NVIDIA is the most extreme case. Revenue jumped from $27.0 billion to $130.5 billion in three years, driven almost entirely by data center GPU demand; the next shipment cycle also revolves around NVIDIA Blackwell [1]. The important caveat: around 85% of NVIDIA revenue comes from six customers: Microsoft, Google, Amazon, Meta, Oracle, and Tesla [8]. GPU buying is highly concentrated among six tech giants, not spread evenly across global enterprises.

A simple analogy helps. During the 1849 California gold rush, the people who sold jeans and pickaxes often made more money than the miners. In this AI wave, NVIDIA sells the picks, the hyperscalers build the roads, and most ordinary companies holding the shovels still have not found the gold mine.

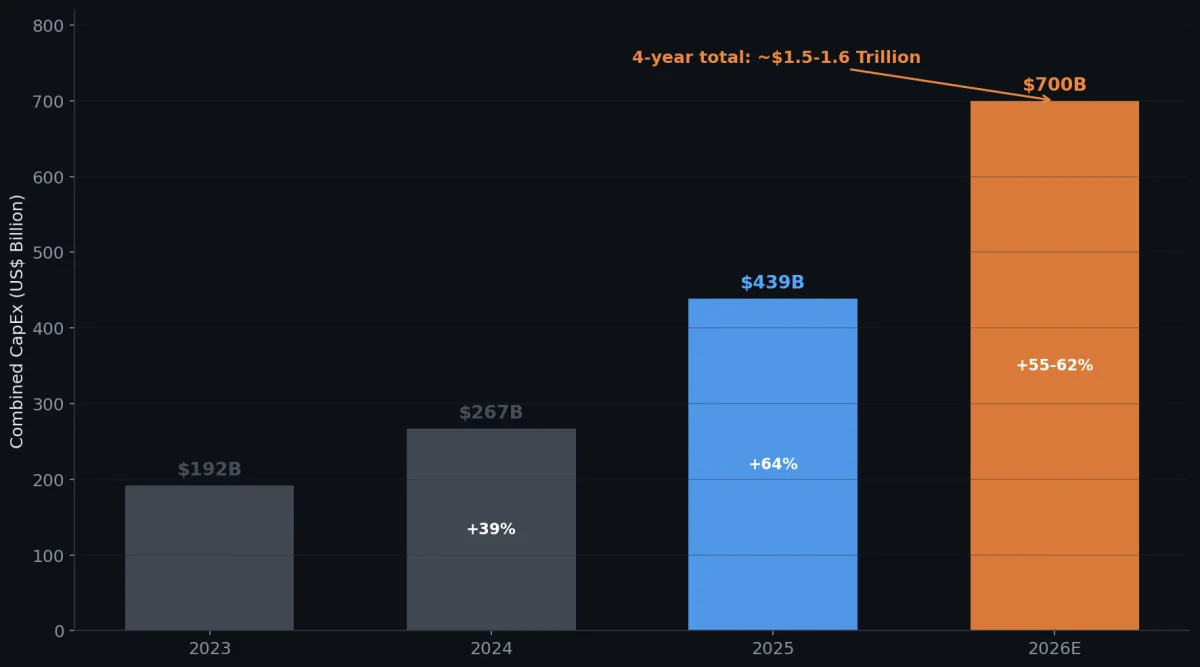

The $700 Billion-a-Year Infrastructure Bet

The main engine behind this market move is capital expenditure, or CapEx: the money tech giants spend on data centers, AI servers, and power infrastructure.

| Year | Combined CapEx of the five hyperscalers | YoY growth |

|---|---|---|

| 2023 | ~$192B | Base year |

| 2024 | ~$267B | +39% |

| 2025 | ~$439B | +64% |

| 2026 guidance | $650-750B | +55-62% |

Sources: Platformonomics [9], Q4 2025 earnings calls from each company [5][6][7][10], Goldman Sachs [11].

From 2023 to 2026, cumulative spending is roughly $1.5 trillion to $1.6 trillion, equal to about 2.2% of U.S. GDP [11]. Amazon’s 2026 guidance alone reaches $200 billion [7], while Alphabet guided for $175-185 billion [6].

This money is changing the asset structure of tech companies. For the past decade, large tech firms were known for being asset-light and high-margin. CapEx usually consumed about 40% of free cash flow [12]. That ratio is now close to 100% [12], and some companies may need debt financing. UBS called this the “AI Profit Gap” in a February 2026 report and downgraded U.S. information technology from “Attractive” to “Neutral” [12].

Société Générale estimates that Meta, Alphabet, and Oracle will need to raise about $86 billion through the bond market in 2026 [8]. Moving from “spend the money we earn” to “borrow to build data centers” is a meaningful structural shift.

That spending ultimately lands in the rack-scale system supply chain, especially Taiwan’s AI server contract manufacturing base, which is why AI CapEx affects more than software-stock multiples.

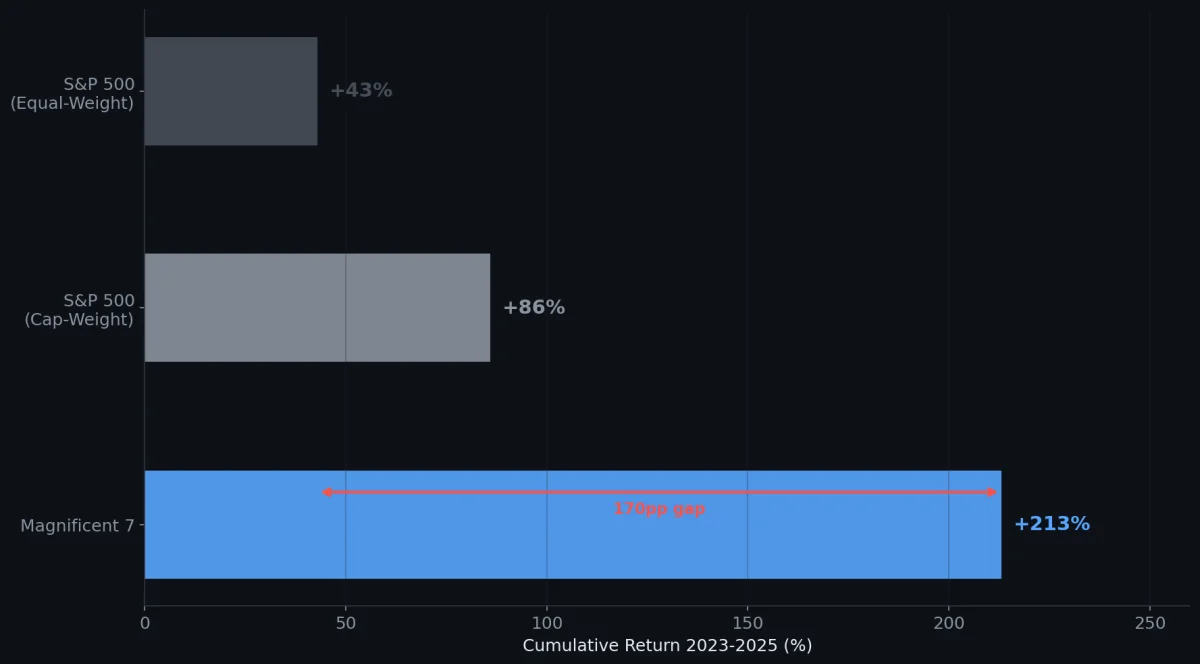

Magnificent 7 Dominance: Both Sides of Concentration

Market gains have been concentrated in a small number of companies. That has been the defining feature of U.S. equities over the past three years.

| Metric | 2023 | 2024 | 2025 | Three-year cumulative |

|---|---|---|---|---|

| Magnificent 7 return | +76% | +48% | +23% | ~213% |

| S&P 500, market cap weighted | +26% | +25% | +18% | ~86% |

| S&P 500 Equal Weight, RSP | +14% | +13% | +11% | ~43% |

Sources: SlickCharts, Capital Group [13], First Trust [14].

The three-year cumulative gap is 43 percentage points, which fully reflects the concentrated contribution of AI-related giants. In 2023, the Mag 7 contributed about 63% of the S&P 500’s total gain, and only 27% of S&P 500 constituents beat the index, the lowest share in nearly 30 years [14].

There were signs of improvement in 2025. The Mag 7 contribution to index gains fell from 63% to 42%, while the other 493 S&P 500 companies rose from 15.7% of index contribution to 58.6% [14]. That may mean AI benefits are starting to spread into broader economic sectors. It may also be a rotation from expensive tech stocks into defensive sectors. For now, we cannot know which one it is.

The Huge Gap Between Adoption and Profit

This is the most consistent finding across the research reports, and it is the biggest question mark for the durability of the AI trade.

McKinsey’s November 2025 survey, covering 1,993 respondents across 105 countries, found [3]:

- 88% of companies use AI in at least one business function, up from 55% in 2023

- 71% regularly use generative AI

- Only 39% attribute any EBIT growth to AI, and most say the contribution is below 5%

- Real AI high performers account for only about 6% of companies

Goldman Sachs senior economist Ronnie Walker was more direct in March 2026: “At the aggregate level, there is still no significant link between AI adoption and productivity.” [15] Goldman chief economist Jan Hatzius also said the actual contribution of AI investment to 2025 U.S. GDP growth was only about 0.2 percentage points [15].

The micro-level data tells a different story. In specific tasks, AI efficiency gains are clear: software engineering task completion rose 26%, junior developer productivity improved 21-40% [16], and core coding efficiency improved 55% [17]. Goldman’s own report also said that among management teams that have quantified AI impact, the median efficiency gain is about 30% [15].

The gap is the conversion from “works at the task level” to “creates profit at the enterprise level.” McKinsey notes that nearly two-thirds of companies remain stuck in pilot mode and do not yet have the ability to deploy AI at scale across departments [3]. Most companies are layering new tools onto old workflows instead of redesigning the workflow itself.

One cost-side change matters: the Stanford HAI report shows that the inference cost of reaching GPT-3.5-level performance fell from $20 per million tokens in November 2022 to $0.07 in October 2024, a 280x drop [16]. Tools are getting cheaper, and the barrier is falling quickly. The question is when the inflection point arrives.

What Are CEOs Saying?

Management comments on earnings calls show how confident executives are about AI-driven revenue.

NVIDIA CEO Jensen Huang, FY26 Q4, 2026-02-25 [1]:

“Compute equals revenues now. Without compute, there is no way to generate tokens. Without tokens, there’s no way to generate revenue.”

Microsoft CEO Satya Nadella, FY25 Q2, 2025-01-30 [2]:

“Our AI business has surpassed an annual revenue run rate of $13 billion, up 175% year-over-year.”

Amazon CEO Andy Jassy, Q4 2025, 2026-02-06 [7]:

“Customers really want AWS for AI workloads. We are monetising capacity as fast as we can install it.”

Meta CEO Mark Zuckerberg, Q4 2025, 2026-01-28 [10]:

“2026 is going to be the year that AI starts to dramatically change the way that we work.”

These are no longer just vision statements. They are tied directly to revenue numbers. Microsoft’s AI business has reached a $13 billion annual revenue run rate [2]. AWS has a $142 billion run rate and a $244 billion backlog [7]. But these numbers are still concentrated on the infrastructure supply side. The profit proof from end-user enterprises remains unfinished.

Penchan’s Observation: What Does the Cross-Consensus Tell Us?

Instead of listening to bulls and bears talk past each other, Penchan thinks the more useful method is to ask: what are the bulls themselves afraid of, and what do the bears themselves admit? That filters out some of the bias and gets us closer to reality.

Three things even the bulls admit:

Citi, the most optimistic major Wall Street bank, acknowledges that five-year spending of $8.9 trillion only recovers $3.3 trillion in revenue, and financing pressure is rising [18]. Morgan Stanley says AI disruption volatility will recur, and 80% of AI benefits come from cost cutting rather than new revenue creation [19]. JP Morgan is even more blunt: “the elements of a bubble are already present,” and the telecom industry’s overbuild of fiber may repeat [20].

In plain English, even people who like AI agree on this: money is being spent too fast, revenue is arriving too slowly, and volatility is certain.

Three things even the bears do not deny:

UBS, the bank that downgraded IT, still lists AI as a “key structural theme” and is adjusting allocation rather than abandoning the theme [12]. Deutsche Bank’s survey shows 57% of investors worry about a crash, but its official S&P 500 target is still 8,000, the highest on Wall Street, and after the selloff it upgraded software stocks back to Overweight [21]. Goldman Sachs says the GDP impact is close to zero, but also explicitly says this is “not yet a bubble” and notes that the Mag 7 P/E is only about half of the 2000 dot-com peak [8].

In practice, even the worried side agrees on this: the AI leaders have real earnings power, nobody thinks investors should completely exit, and buyers show up after drawdowns.

The conclusion after crossing both sides:

- AI is a real technology shift, but market pricing may be ahead of value realization

- There is no need to panic-sell, but the risk of overconcentration in tech stocks is now a consensus concern

- Volatility is almost certain, and timing risk may be higher than directional risk

- 2026 to 2028 is the key validation window. Sequoia Capital’s $500 billion annual revenue gap needs to be filled during this period [22]

- Every major bank mentions sector rotation, which implies the next-stage AI beneficiaries may not be the same companies that already rose the most

These are observable market consensuses from public research reports, not personal investment advice. Your own allocation decision comes down to one question: can the revenue curve catch up with the investment curve before 2028?

References

[1] NVIDIA, “NVIDIA Announces Financial Results for Fourth Quarter and Fiscal 2025,” NVIDIA Newsroom, 2025-02-26. https://nvidianews.nvidia.com/news/nvidia-announces-financial-results-for-fourth-quarter-and-fiscal-2025

[2] Microsoft, “FY25 Q2 Earnings Press Release,” Microsoft Investor Relations, 2025-01-29. https://www.microsoft.com/en-us/investor/earnings/fy-2025-q2/press-release-webcast

[3] McKinsey & Company, “The State of AI in 2025: Agents, Innovation, and Transformation,” McKinsey Global Survey, 2025-11-05. https://www.mckinsey.com/capabilities/quantumblack/our-insights/the-state-of-ai

[4] MIT Sloan School of Management, “Why Most GenAI Pilots Fail to Deliver Business Value,” MIT Working Paper, 2025-08.

[5] Alphabet, “Alphabet Earnings Q4 2025: CEO’s Remarks,” The Keyword (Google Blog), 2026-02-04. https://blog.google/company-news/inside-google/message-ceo/alphabet-earnings-q4-2025/

[6] Alphabet, “Q4 2025 Earnings Call Transcript,” Alphabet Investor Relations, 2026-02-04. https://abc.xyz/investor/

[7] Amazon, “Amazon.com Announces Fourth Quarter Results,” Amazon Investor Relations, 2026-02-05. https://ir.aboutamazon.com/news-release/news-release-details/2025/Amazon-com-Announces-Third-Quarter-Results/

[8] Goldman Sachs, “AI: In a Bubble?” Top of Mind, Issue 143, 2025-10-28. https://www.goldmansachs.com/pdfs/insights/goldman-sachs-research/ai-in-a-bubble/report.pdf

[9] Platformonomics, “Follow the CAPEX: 2025 Retrospective,” 2026-02-25. https://platformonomics.com/

[10] Meta Platforms, “Q4 2025 Earnings Call Transcript,” Meta Investor Relations, 2026-01-28. https://s21.q4cdn.com/399680738/files/doc_financials/2025/q4/META-Q4-2025-Earnings-Call-Transcript.pdf

[11] Goldman Sachs, “Why AI Companies May Invest More than $500 Billion in 2026,” Goldman Sachs Insights, 2025-12-18. https://www.goldmansachs.com/insights/articles/why-ai-companies-may-invest-more-than-500-billion-in-2026

[12] UBS, “Downgrading US Information Technology,” UBS CIO Daily, 2026-02-10. https://www.ubs.com/global/en/wealthmanagement/insights/chief-investment-office/house-view/daily/2026/latest-10022026.html

[13] Capital Group, “Beyond the Magnificent Seven,” Capital Group Insights, 2025. https://www.capitalgroup.com/pcs/insights/articles/magnificent-seven-chart-diversify.html

[14] First Trust, “The S&P 500 Index in 2024: A Market Driven Once Again by the Mag 7,” First Trust Economic Research, 2025-01-08. https://www.ftportfolios.com/Commentary/EconomicResearch/2025/1/8/the-sp-500-index-in-2024-a-market-driven-once-again-by-the-mag-7

[15] Goldman Sachs, “Will AI Eat Software?” Goldman Sachs Research, 2026-03-09. (Goldman Sachs client-only report; figures cited from public references in Fortune 2026-03-03 and Bloomberg 2025-12-12)

[16] Stanford University, “AI Index Report 2025,” Stanford HAI, 2025-04-07. https://aiindex.stanford.edu/report/

[17] Accenture, “Developer Productivity Study with GitHub Copilot,” Accenture Technology Vision, 2025. (Figure cited from public references in Microsoft FY26 Q2 Earnings Call, 2026-01)

[18] Reuters, “Citigroup raises AI capex and revenue forecasts amid rapid enterprise adoption,” Reuters, 2026-03-10. https://www.reuters.com/technology/citigroup-raises-ai-capex-revenue-forecasts-amid-rapid-enterprise-adoption-2026-03-10/

[19] Morgan Stanley, “Mapping AI’s Rate of Change: Where the Rubber Meets the Road,” Morgan Stanley Research, 2026-02-11. https://www.morganstanley.com/content/dam/msdotcom/en/assets/pdfs/Research_AI-Rate-of-Change.pdf

[20] J.P. Morgan Private Bank, “Outlook 2026: Promise and Pressure,” 2025-11-17. https://assets.jpmprivatebank.com/content/dam/jpm-pb-aem/global/en/documents/outlook2026/JPMorganOutlook2026PromiseandPressure.pdf

[21] Deutsche Bank, “Your Biggest Risks for 2026,” DB Thematic Research, 2025-12. https://prod1.www.dbresearch.com/PROD/RI-PROD/PROD0000000000613003/

[22] Sequoia Capital, David Cahn, “AI’s $600B Question,” Sequoia Capital Blog, 2024-06-20. https://www.sequoiacap.com/article/ais-600b-question/

Penna 🐧 · penchan.co · 2026.03.28